The AI Boom Has a Debt Problem

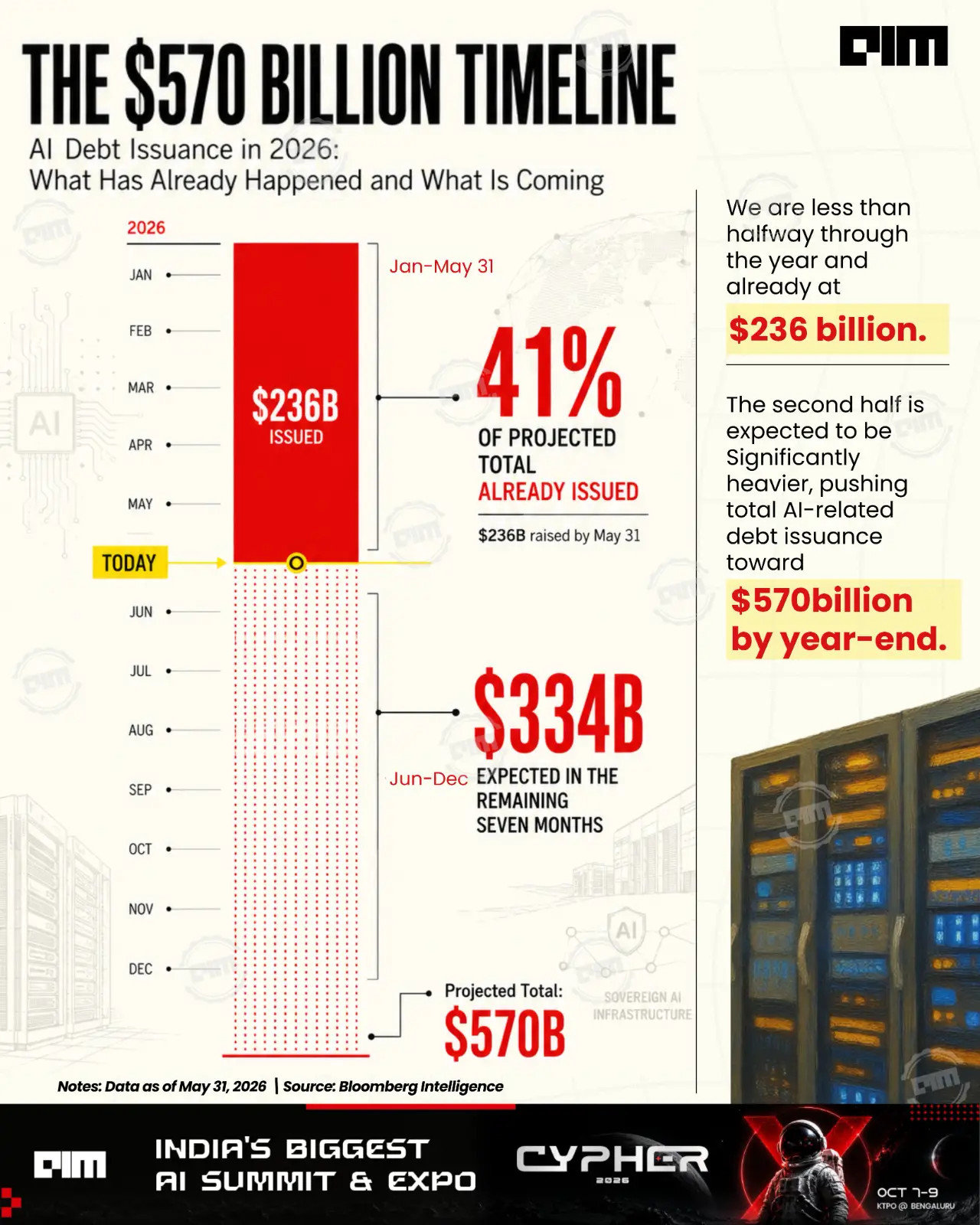

Morgan Stanley forecast that AI-related global debt issuance will reach nearly $570 billion this year.

In 2026, the most consequential shift in global capital markets is happening in bonds, and it is being driven entirely by AI.

On June 10, 2026, Morgan Stanley forecast that AI-related global debt issuance will reach nearly $570 billion this year, more than doubling from 2025 levels. As of May 31, $236 billion had already been issued, a fourfold increase over the same period last year.

The pace of issuance in the first five months of 2026 alone exceeds total AI-related bond issuance in any previous full year, as claimed by Morgan Stanley.

This is a debt born of necessity, not ambition. Alphabet carries an AA+ credit rating. Meta carries AA-. Amazon carries AA. These are among the strongest balance sheets in corporate history.

According to the report, they are borrowing because the scale of AI infrastructure investment has grown large enough that even their cash flows, which run into the hundreds of billions annually, cannot absorb it without depleting the financial reserves that investors expect them to maintain.

As Finimize, the UK-based financial information and media platform, put it in its analysis of the Morgan Stanley report, AI is moving from a software theme to a financing cycle.

How the Shift Happened

The scale of the change in hyperscaler borrowing behavior is visible in a single BofA Securities data point. The Big Five hyperscalers including Amazon, Alphabet, Microsoft, Meta, and Oracle, issued $121 billion in US corporate bonds in 2025 alone.

Their annual average between 2020 and 2024 was $28 billion. That is a 4x increase in one year, from companies that had previously relied almost entirely on operating cash flows to fund growth.

The driver is AI capex. Hyperscalers Alphabet, Amazon, Microsoft, and Meta are expected to spend a combined $700 billion in capital expenditures in 2026, covering data centers, servers, chips, energy infrastructure, and the interconnected physical systems that make large-scale AI training and inference possible. That figure is projected to surpass $1 trillion in 2027.

To put the trajectory in context: Gartner estimates that worldwide AI spending will reach $2.52 trillion in 2026, a 44% year-over-year increase, according to M&G Investments.

Total AI spending between 2013 and 2024 was $1.6 trillion. The same amount is now being deployed in roughly one year.

BofA analysts expect the Big Five to borrow approximately $140 billion annually over the next three years, with the figure potentially exceeding $300 billion annually as AI infrastructure needs intensify.

Morgan Stanley expects issuance to ramp further in the second half of 2026, as the hyperscaler capex cycle accelerates into year-end.

>

>The Bond Market Transformation

The volume of AI-related issuance is large enough to structurally alter the composition of global credit markets, as per Morgan Stanley.

Vontobel estimates that AI or data center-related bond issuance could reach $300 billion over the next year and approximately $1.5 trillion over the next five years.

At that scale, AI-related bonds would represent 15-20% of most corporate bond indices, larger than the US banks component in some indices.

Christian Hantel, Head of Global Corporate Bonds at Vontobel, described the issuance trend as "only likely to accelerate further in 2026," after AI-related investments already accounted for approximately 30% of total net issuance in the US dollar-denominated investment grade market in 2025.

Barclays forecasts total US corporate bond issuance to reach $2.46 trillion in 2026, up 11.8% from $2.2 trillion in 2025, with net issuance rising 30% to $945 billion. Its analysts describe the biggest upside risk to supply as AI hyperscaler capex, which "could require more jumbo public deals than typical."

Hyperscalers are also broadening their investor base beyond US dollar markets, issuing bonds in euros, sterling, and other currencies to access deeper pools of capital and diversify their funding sources across geographies.

The Absorption Question

The structural argument for AI-related bonds is simple. The companies issuing them have the strongest credit ratings in the market, predictable and growing cash flows, and a demonstrated ability to service debt at scale. The absorption question is different, and Morgan Stanley flags it directly.

"Fundamental backdrop remains strong," Morgan Stanley noted in its June 10 report, "but for now we think price action is being mostly driven by supply expectations."

When issuance calendars run heavy, investment-grade borrowers typically need to offer new-issue concessions, extra yield relative to existing bonds already trading, to clear deals at the volumes they require.

Those concessions lift borrowing costs even for AA-rated companies and can widen credit spreads more broadly as the market digests the volume.

Tighter financial conditions in credit markets can constrain companies in the AI supply chain that depend on steady access to debt markets but lack hyperscaler-grade credit ratings.

This can include chip manufacturers, data center operators, energy infrastructure providers, and the broader network of suppliers building the physical layer beneath the AI model layer.

The hyperscalers can absorb wider spreads. Their suppliers may not be able to as easily. And the heaviest issuance is still ahead.

Morgan Stanley expects the second half of 2026 to be busier than the first, as hyperscaler capex cycles accelerate into year-end and the $570 billion forecast becomes a floor rather than a ceiling. The bond market has barely begun to absorb the AI buildout.

Key Takeaways

- Forecast AI-related global debt issuance will reach nearly $570 billion in 2026, doubling from 2025.

- Major companies like Alphabet and Meta are borrowing to fund massive AI infrastructure investments.

- Issuance pace in 2026 surpasses total AI-related bonds issued in any previous full year.

- Shift indicates AI is evolving from software development to a significant financing cycle.

- Strong corporate balance sheets are being leveraged to avoid depleting financial reserves.